April 2024 Manufacturing Business Outlook Survey

Note: Survey responses were collected from April 8 to April 15.

Manufacturing activity in the region continued to expand this month, according to the firms responding to the April Manufacturing Business Outlook Survey. The survey’s indicators for general activity, new orders, and shipments all rose. However, the employment index remained negative. Both price indexes continue to suggest overall price increases. Most future activity indicators declined but continue to suggest that firms expect growth over the next six months.

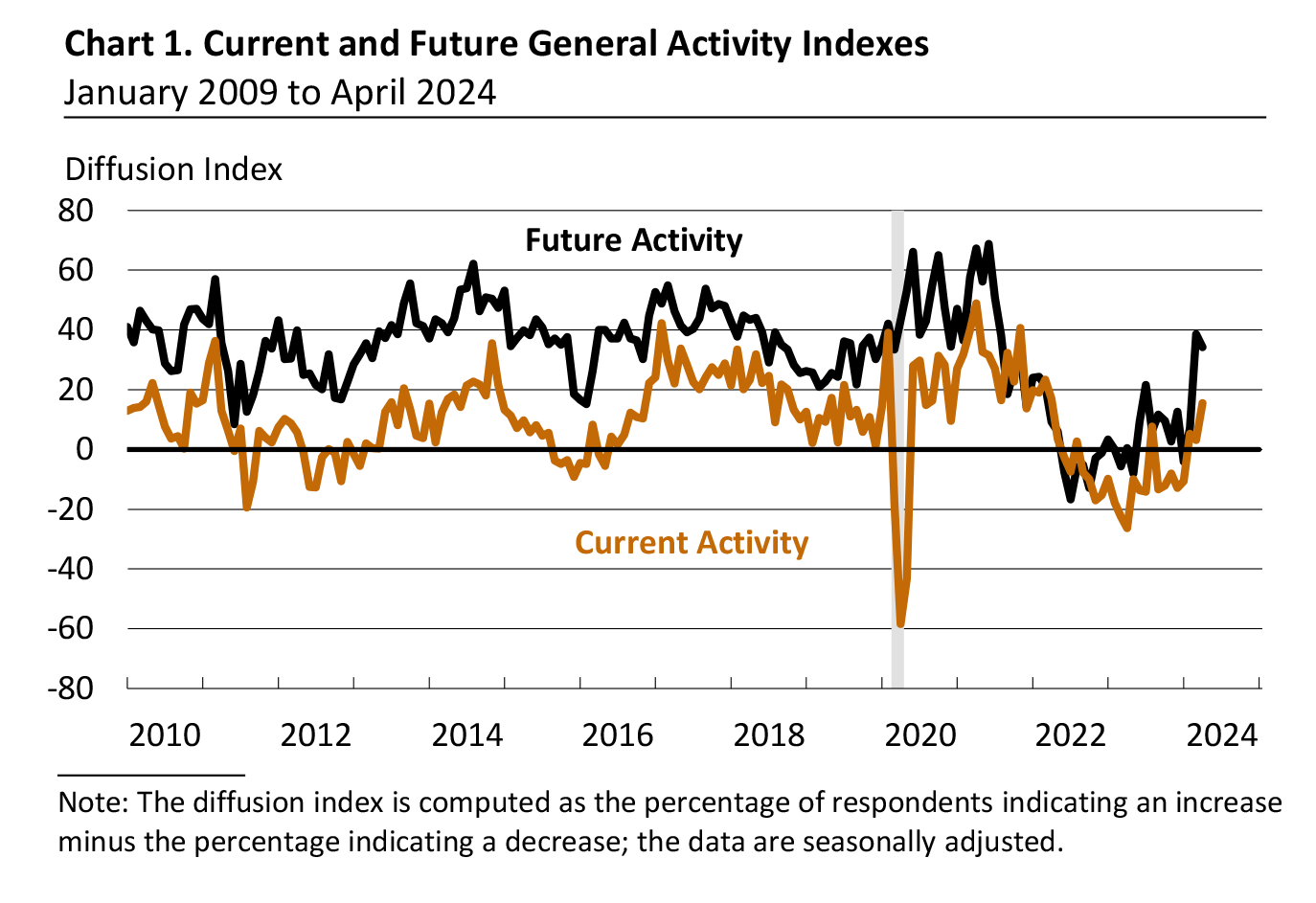

Current Indicators Improve This Month

The diffusion index for current general activity rose 12 points to 15.5 in April, its third consecutive positive reading and highest reading since April 2022 (see Chart 1). Almost 38 percent of the firms reported increases in general activity this month, while 22 percent reported decreases; 40 percent reported no change. The index for new orders increased 7 points in April, its second consecutive positive reading. The current shipments index rose 8 points to 19.1 this month.

The firms continued to report an overall decline in employment. The employment index edged down 1 point to -10.7 in April, its 12th negative reading in the past 14 months. Most firms (77 percent) continued to report no change in employment, while the share of firms reporting decreases (16 percent) exceeded the share reporting increases (6 percent). The average workweek index fell further, from -0.2 to -18.7.

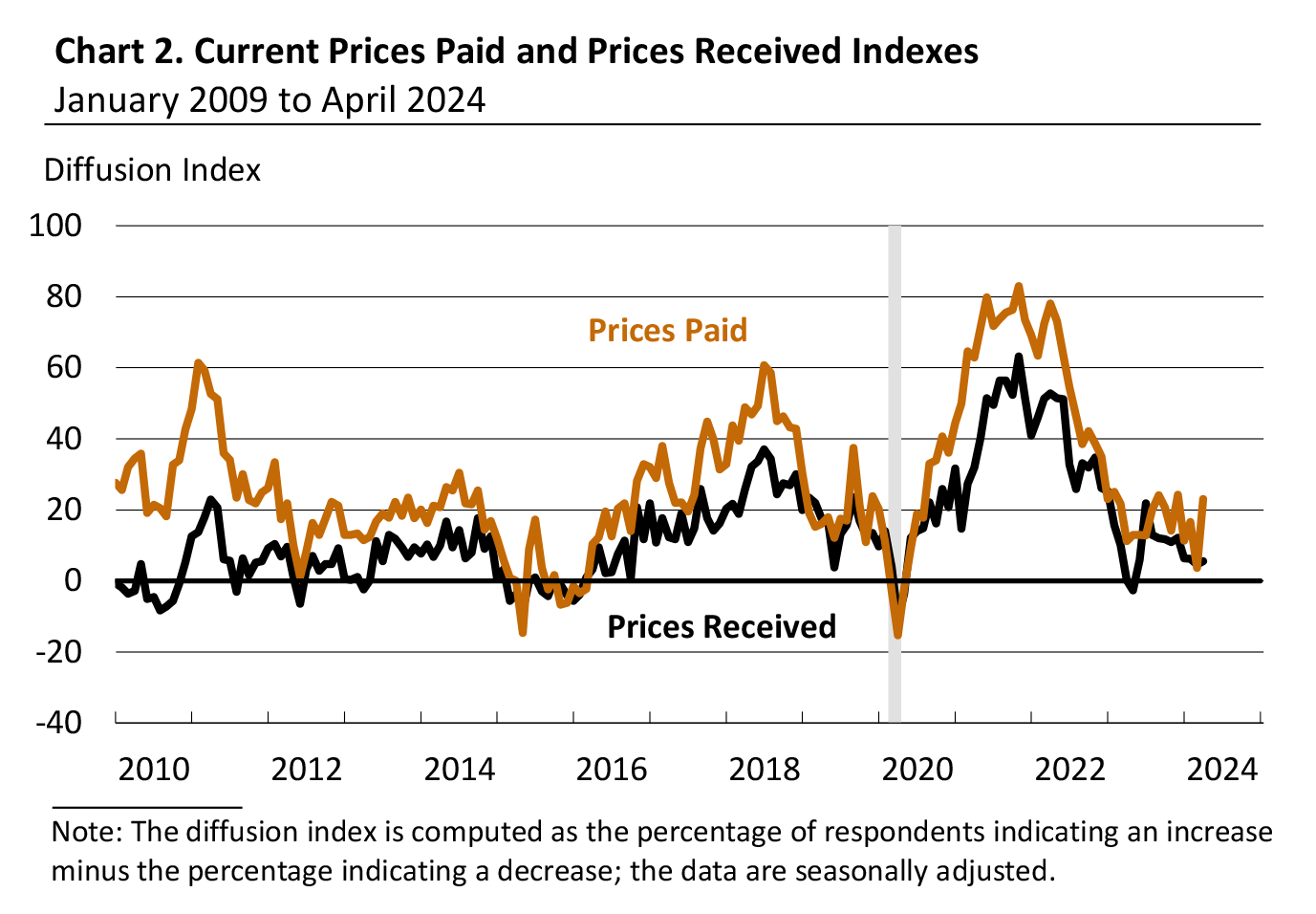

Firms Continue to Report Overall Price Increases

The prices paid index jumped from 3.7 in March to 23.0 in April, its highest reading since December 2023 and near, but below, its long-run average (see Chart 2). Almost 26 percent of the firms reported increases in input prices (up from 14 percent last month), while 3 percent reported decreases (down from 10 percent); 70 percent reported no change (down from 75 percent). The current prices received index ticked up 1 point to 5.5. Almost 12 percent of the firms reported increases in the prices of their own goods, 6 percent reported decreases, and 82 percent reported no change.

Firms Continue to Expect Increases for Wages

In this month’s special questions, the firms were asked about changes in wages and compensation over the past three months, as well as their updated expectations for changes in various input and labor costs for the current year. More than 31 percent of the firms indicated wages and compensation costs had increased over the past three months, 69 percent reported no change, and none reported decreases. Most firms (78 percent) reported not needing to adjust their 2024 budgets for wages and compensation since the beginning of the year; however, equal shares of the respondents (9 percent) are planning to increase wages and compensation by more than originally planned, and sooner than originally planned.

The firms still expect cost increases across all categories of expenses in 2024, and the median expected increases were in line with or slightly higher than expectations for most categories when this question was last asked in July. The responses indicate a median expected increase of 3 to 4 percent for wages and of 4 to 5 percent for total compensation (wages plus benefits), both unchanged from July.

Future Indicators Remain Positive

The diffusion index for future general activity declined from 38.6 in March to 34.3 in April (see Chart 1). Forty-four percent of the firms expect an increase in activity over the next six months, exceeding the 10 percent that expect a decrease; 39 percent expect no change. The future new orders index decreased 7 points to 42.8, and the future shipments index fell 14 points to 29.3. The firms expect an increase in employment over the next six months: The future employment index increased from a reading of 5.8 in March to 12.8 this month. The future prices paid index moved up to 54.5, while the future prices received index fell 3 points to 34.4. The index for future capital expenditures fell 4 points to 20.0.

Summary

Responses to the April Manufacturing Business Outlook Survey continued to suggest an overall increase in regional manufacturing activity this month. The indicators for current activity, new orders, and shipments rose. The firms continued to indicate an overall decline in employment, and the current price indexes suggest overall price increases. The survey’s broad indicators for future activity fell but remained positive, suggesting continued expectations for growth over the next six months.

Special Questions (April 2024)

|

|

Percent (%) |

|---|---|

| Increased | 31.3 |

| No change | 68.7 |

| Decreased | 0.0 |

|

|

Percent (%) |

|---|---|

| Yes, and we are planning to increase wages and compensation by more than originally planned. | 9.4 |

| Yes, and we are planning to increase wages and compensation sooner than originally planned. | 9.4 |

| No, we have not needed to make adjustments. | 78.1 |

| Other | 6.3 |

| *Percentages do not sum to 100 because more than one option could be selected. | |

| Energy (%) |

Other Raw Materials (%) |

Intermediate Goods (%) |

Wages (%) |

Health Benefits (%) |

Nonhealth Benefits (%) |

Wages + Health Benefits + Nonhealth Benefits (%) | |

|---|---|---|---|---|---|---|---|

| Decline of more than 1% | 6.5 | 6.7 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| No change | 16.1 | 16.7 | 30.0 | 12.9 | 22.6 | 27.6 | 6.9 |

| Increase of 1–2% | 12.9 | 3.3 | 10.0 | 0.0 | 6.5 | 13.8 | 3.4 |

| Increase of 2–3% | 25.8 | 30.0 | 30.0 | 12.9 | 16.1 | 24.1 | 13.8 |

| Increase of 3–4% | 12.9 | 13.3 | 3.3 | 58.1 | 3.2 | 13.8 | 17.2 |

| Increase of 4–5% | 16.1 | 16.7 | 20.0 | 16.1 | 19.4 | 17.2 | 31.0 |

| Increase of 5–7.5% | 6.5 | 3.3 | 3.3 | 0.0 | 12.9 | 0.0 | 13.8 |

| Increase of 7.5–10% | 0.0 | 6.7 | 0.0 | 0.0 | 6.5 | 3.4 | 6.9 |

| Increase of 10–12.5% | 3.2 | 3.3 | 3.3 | 0.0 | 9.7 | 0.0 | 6.9 |

| Increase of more than 12.5% | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Median Expected Change | 2–3% | 2–3% | 2–3% | 3–4% | 3–4% | 2–3% | 4–5% |

| Median Expected Change (July 2023) | 1–3% | 2–3% | 2–3% | 3–4% | 4–5% | 1–2% | 4–5% |

| **The firms responded to more detailed changes than shown in the provided ranges. | |||||||

Return to the main page for the Manufacturing Business Outlook Survey.